See all results for ''

Evolution fascinates me. Nature, people, industries and most of all, society. In the latest episode of the podcast ‘99% Invisible’, Roman Mars asks an ingenious question: ‘why did humans organise things in alphabetical order and why are alphabets arranged in the sequence they are?’ I never paused to think of that. Its a podcast worth your while.

In a similar vein, norms of social behaviours we take for granted today were unacceptable a generation ago. 20 odd years ago, smoking in airplanes was the norm. Even more recently, smoking in restaurants and public spaces was acceptable. The same goes for the investment industry. When we look back a couple of generations ago, the landscape was much simpler. Access to information was limited. You invested in local or regional businesses and usually less complicated ones. Long-term steady appreciation, safety and regular income motivated savers. Over time, society morphed, businesses became global, and technology spurred changes. Individual investors gave way to ‘professionals’. At first, mutual funds and then subsequently ETF’s became the dominant form of investing in markets. COVID changed this trend – at least for now. Communities on Reddit empowered individuals to take back control. Easy liquidity made investing look easy. Investors became traders. 'HODL' and investment memes took off. Blockchain, crypto, Bored Apes, Axie Infinity and insane volatility. Concurrent with this phase is the prominence afforded to commentators.

‘Experts’ are indispensable in our industry. They now live at the intersection of knowledge (often superficial), experience (not necessary) and communication (articulate but the weirder the better). Expressing an opinion is paramount. Atomised in 240 characters or as a 30-second TikTok video. At every price action, we have a ready explanation. Alacrity is paramount, achieving a viral status the motive.

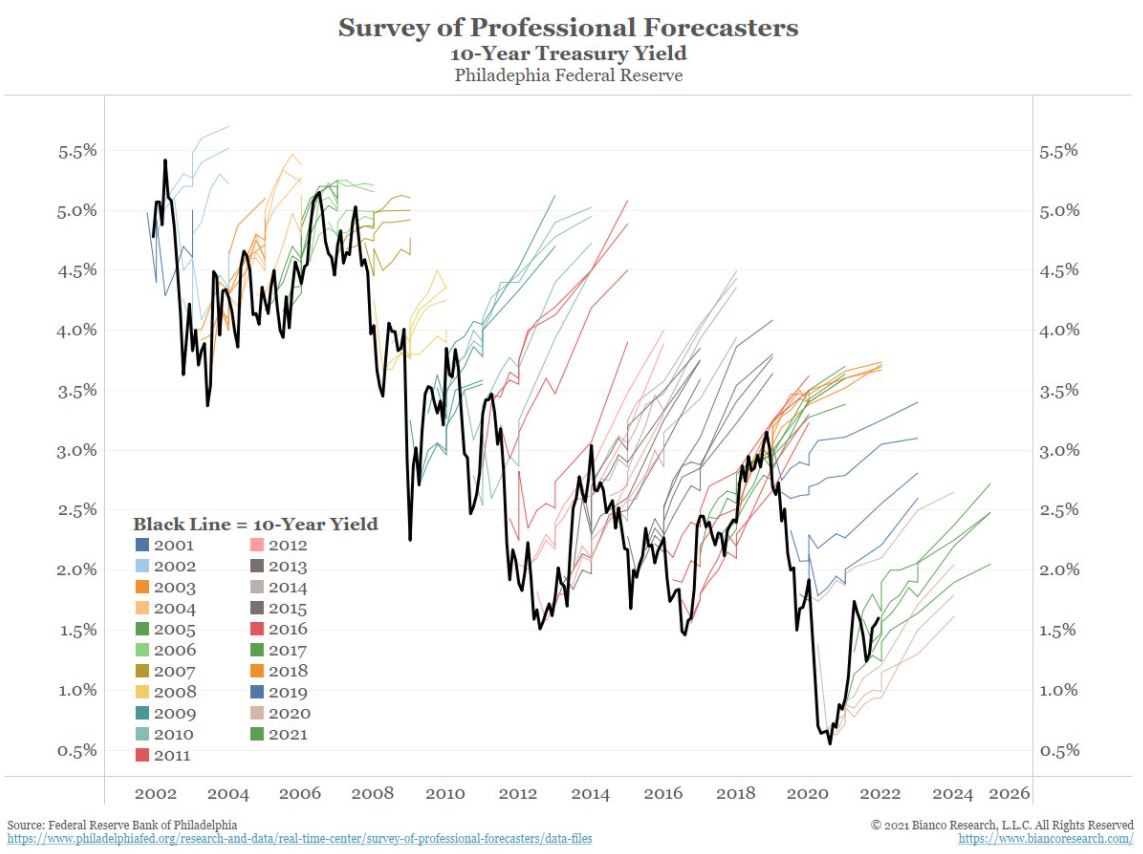

As the new COVID variant roiled markets, there is a reassessment of risks in the market. Mr. Powell’s elegant about turn, retiring transitory from his lexicon when describing inflation, complicates matters. For months, the FED tried to convince the market they were on top of things – inflation in particular. Their crystal ball it seemed, with little doubt, predicted a return to low inflation. Markets were sanguine; the experts were unconvinced. Treasury bond yield forecasts from the Society of Professional Forecasters (the oldest quarterly survey of macroeconomic forecasts in the United States conducted by the Federal Reserve Bank of Philadelphia) were adamant rates were heading higher.

Hang on – do you notice the anomaly? Year in, year out for the past two decades, America’s top economists have predicted that bond yields will rise. They have, by-and-large, been wrong. To appear knowledgeable you confidently project a persona. That done, you move on to the next forecast. Do these experts ever look back at their predictions?

At this moment of uncertainty, I confess bafflement. Both sides of the argument on interest rates and inflation (predicting higher or lower) persuade me. It seems rational to consider the possibility of higher inflation and hence higher interest rates. As individuals, we experience rising prices across the board. Companies in Asia too have mentioned rising costs. In the US, strong demand conditions coupled with a lack of adequate staff have led to higher wages.

Yet we were in a similar situation in the past. Those in the deflationary camp point to high levels of debt and technological advancements keeping a lid on price increases. Japan has tried almost everything, yet inflation has barely budged over the past decade or more. Those forecasts for rising rates – haven’t we seen them before? In this tug of war, I have no clue as to which way rates will go.

A simple approach is to use a “barbell strategy” where a portfolio is weighted to opposing outcomes. Since I have no strong conviction on outcomes, hedge your bets. If the 10-year bond yield does rise, invest part of your portfolio in companies, which have lower correlation to the adverse impacts of rising rates. In my opinion, Southeast Asia likely fits the bill. Southeast Asia is neglected, out of favour and cheap. Countries like Indonesia Singapore and the Philippines are benefiting from the reflation.

China should also be back on the list in a barbell approach. Stocks in China have been a massive disappointment. The Chinese Communist Party’s enforcement of their ideological direction combined with excess optimism reflected in high valuations at the start of the year did not help. The good news in my opinion is that we have a clearer indication of what the CCP wants businesses to focus on. It’s a little easier to state what not to invest in. Shares in Alibaba are amongst the worst performing stocks this year. Yet Alibaba is not representative of China as a whole. There are opportunities and I think it is important to keep an open mind.

In the past 18 months, China’s central bank acted in a diametrically opposite manner to other central banks; the PBoC was tightening monetary policy. First deflating the peer-to-peer (shadow) lending networks and now assisting a crackdown on the property sector in deflating that bubble. Clearly, this is putting a strain on GDP growth. The next few months are likely to be far more challenging on the growth front with unintended consequences. Earnings growth for broad corporate China is under pressure. Yet, if global yields do rise, could we anticipate the PBoC doing the opposite of the FED and loosening monetary policy? Should we be alive to the fact that liquidity conditions in China might turn benign at a time when the rest of the world is quite negative on China? I started dipping my toes into the water by buying a few idiosyncratic stocks.

The other side of the barbell in a well-structured portfolio are companies that should thrive irrespective of whether inflation proves transitory. There may be valuation risks with some of these names, but a barbell requires me to assume that risk if the other end of the spectrum has cheaper and out of favour stocks. I want to have some part of my portfolio in structural winners in case forecasts of rising interest rates based on rising inflation turns out to be wrong. There are no easy answers during times of uncertainty. Just ask the Society of Professional Forecasters.

Disclaimer

Past performance is no guarantee of future performance. This is a marketing communication. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. Investing in companies in emerging markets involves higher risk than investing in established economies or securities markets. Emerging Markets may have less stable legal and political systems, which could affect the safe-keeping or value of assets. The Fund’s investments may include shares in small-cap companies and these tend to be traded less frequently and in lower volumes than larger companies making them potentially less liquid and more volatile. The information contained herein including any expression of opinion is for information purposes only and is given on the understanding that it is not a recommendation. Information on the rights of investors can be found here.

Samir Mehta, manager of the JOHCM Asia ex Japan fund, provides an in-depth look at Jubilant Foodworks, the largest holding in his portfolio.

Taking stock: Samir Mehta, manager of the JOHCM Asia ex Japan Fund, takes a look back at markets over the last 18 months.

What next for China? Samir discusses the regulatory clampdown including two other sectors not yet hit - housing and healthcare.

For a better experience, we recommend viewing this website in landscape orientation.