See all results for ''

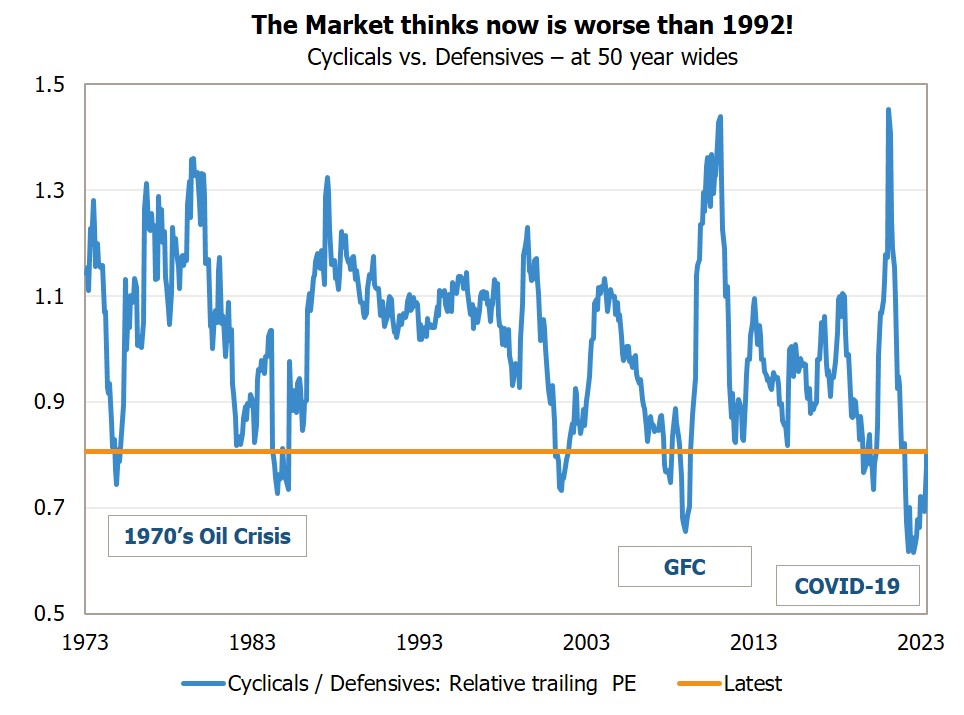

The UK stock market has a value bias. Since 2008, through what proved to be a prolonged period of low interest rates and extraordinary levels of liquidity, being on the value side of the dial has been a disadvantage.

Interest rates are not high by historic standards but they are significantly higher than many of us are used to and likely to remain positive for the longer term. Should that mean a more optimistic outlook for UK equities? If so, it doesn’t seem to be happening yet. A glance at a selection of stocks shows multiples that are still in the basement. Based on recent consensus forecasts for 2023, BP is expected to trade on a P/E of 6, Kier on 4, NatWest on 5.7, Aviva on 7.2. And yet no one suggests that any of these companies are struggling.

In a recent webinar, we looked in more depth at three companies in our portfolio, hoping to explain why currently multiples make little intrinsic sense. Access the full webinar here.

Standard Chartered

This is a UK bank the majority of whose business is in Asia. Over a third of its assets are in China, followed by Singapore and Korea. Like other banks, it is benefiting from higher interest rates while steering its business to less capital-intensive revenue streams, such as wealth management. It’s return on equity in 2024 is forecast to be over 11%, while its P/E is expected to be under 5x.

easyJet

Several factors continue to hold back the full recovery of the airline sector, from staff shortages to delays in equipment delivery. But recovery is still pushing forward and traffic should be back to pre-Covid levels by 2025. Fare revenue is as good as it has ever been, while ancillary revenue is nearly double what it was pre-pandemic and is expected to continue to grow.

Keller

Keller is the world’s largest ‘geotechnical’ specialist contractor. It does things like put piles in the ground to form the foundations of buildings. It is expected to do well from infrastructure required for onshoring and decarbonisation. It is working on three LNG terminals in the Gulf of Mexico and expects £130 million in sales for the NEOM project in Saudi Arabia. It is currently on a P/E of 6x and dividend yield of 6%

Disclaimer

Professional investors only. This is a marketing communication. Please refer to the fund prospectus and to the KIID / KID before making any final investment decisions. The investment promoted concerns the acquisition of shares in a fund or the investment strategy and not the underlying assets. Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. The information contained herein including any expression of opinion is for information purposes only and is given on the understanding that it is not a recommendation. The information in this article does not constitute, or form part of, any offer to sell or issue, or any solicitation of an offer to purchase or subscribe for any funds or strategies described in this article; nor shall this article, or any part of it, or the fact of its distribution form the basis of, or be relied on, in connection with any contract.

Source: JOHCM (unless otherwise stated.)

UK inflation exceeded expectations, but the Fund offers attractive growth and robust dividends

Are we overly pessimistic on the underlying resilience of the UK economy? Are we reading too much into headline inflation and over-discounting more positive data?

The UK economy defies sceptics with upgraded forecasts, improved labour supply and resilient sectors

For a better experience, we recommend viewing this website in landscape orientation.