See all results for ''

As an asset class, Europe ex UK has been overlooked by investors for years, dismissed as cyclical and value-biased, an old economy. But the burgeoning thematic opportunities presented by recent EU initiatives and the internationalisation of the Continental stock exchanges put European equities firmly back on the map. If analysts and investors have spent years overlooking Europe, we think they’d be wise to start looking it over once again.

A changing index

The years 2011 to 2019 saw barely any earnings growth in Continental Europe, as the ills of the great financial crisis were slowly repaired. As equity markets are powered by earnings, this meant many investors took scant interest. But earnings growth in Europe has recovered strongly in the post pandemic period, outpacing growth in the US and globally. That’s partially because the higher growth sectors, like tech, healthcare and luxury, now represent a bigger part of the Europe ex UK index, while the predominance of the slower, old economy sectors, has declined.

Europe ex UK index exposure to healthcare and tech stocks has risen by 7.3% and 4.7% respectively since June 2009, with financials and telecoms falling 7.2% and 4.6% respectively. Of the ten biggest market capitalisation stocks in Europe ex UK in June 2009, only two remain in the top ten: Nestle and Roche. LVMH and Novo Nordisk have bumped the likes of Santander and Telefonica right down the list. These changes mean today’s index is intrinsically higher growth. Not only does that improve the prospects of higher earnings growth in future, and with that, higher returns on equity. It also means the index will be less cyclical as these higher growth sectors tend to have stronger structural underpinning.

Europe becomes more thematic

There’s major change afoot in Continental Europe. The EU’s Green Deal was signed in 2019, with the primary aim of making Europe the first net zero continent by 2050. The deal also promises to transform the EU into a modern, competitive economy, stating ‘no person and no place will be left behind’. Homes will be more energy efficient and nature will be better protected. The deal was written into EU climate law a couple of years later, with the additional target of reducing net greenhouse gas emissions by at least 55% by 2030.

The Russian invasion of Ukraine has given an added sense of urgency to plans to reform Europe’s energy infrastructure. Another initiative, REPowerEU, followed the invasion and aims to make the energy demands of the EU self-sustainable, bringing yet more investment to renewable energy.

By the very nature of these grand targets and investments, they affect every single sector. It isn’t just about decarbonisation. These initiatives radically alter the EU’s growth trajectory, positioning the trade-bloc as the global leader in environmental technologies. To put it in investment terms, this makes it a multi-sectoral thematic opportunity with the potential for years of strong returns; not how many analysts would have described the region over the past decade.

Schneider is a great example of a European green deal leader, a company at the heart of the energy transition. The decarbonisation of the energy supply is addressed by Schneider’s renewable power supply management solutions, whilst the need for greater energy efficiency in buildings is targeted by the companies’ energy monitoring, temperature control and lighting control products. Schneider expects electricity consumption to rise four-fold globally from 2020 to 2040 and here its EV charging solutions and heat pumps will help to expedite the transition.

RWE is another example. It continues on its metamorphosis into a green giant, being a key contributor to Germany’s target of deriving 80% of energy needs from renewables by 2030. The legacy of its lignite driven past is steadily being left behind. Whilst proving to be of crucial help after Russia halted gas supplies in the summer of 2022, all of RWE’s coal fired power stations will be closed over the next seven years. Meanwhile RWE is now the second largest global offshore wind player and targets 50GW of green installed net capacity by 2030.

Further change was wrought by the 2020 EU Next Generation Recovery plan (the EU’s response to Covid), worth around €750 billion, and split 40% on the green transition and 30% on digital transformation. These digital plans include EU-wide ultra-fast broadband, digital identities to allow more control over personal data, and greater use of artificial intelligence to fight climate change, improve healthcare, transport, and education. EU-funded training courses will allow everyone to improve their digital skills. These changes will bring Continental Europe to the forefront of global digital initiatives.

Europe benefits from a number of digital leaders, not least with the likes of Cap Gemini which recently signed a generative AI partnership with Google and remains a key enabler of corporates digital pathways. ASML continues to have a near monopoly in leading edge lithography, where demand for its products is underpinned by the global megatrends in the electronics industry. The reshoring of semiconductor fabs, as companies seek to source key components closer to home, will drive demand both in Europe and the US.

Compelling Valuations

European companies increased global exposure gives even greater support to growth. The top 10 stocks in Europe ex UK, on an index weighted basis, source 74% of their revenue from outside Europe, and we expect that proportion to rise. Companies like Novo Nordisk, now the world’s third largest pharmaceutical company, are seeing strong globally driven demand for its products. That means there’s a broader internationalisation of the European stock index, where the ex-Europe revenue percentage has risen by 10% from 2007 to 55%. As these behemoths are being favourably exposed to global thematics. Europe is in effect becoming less European.

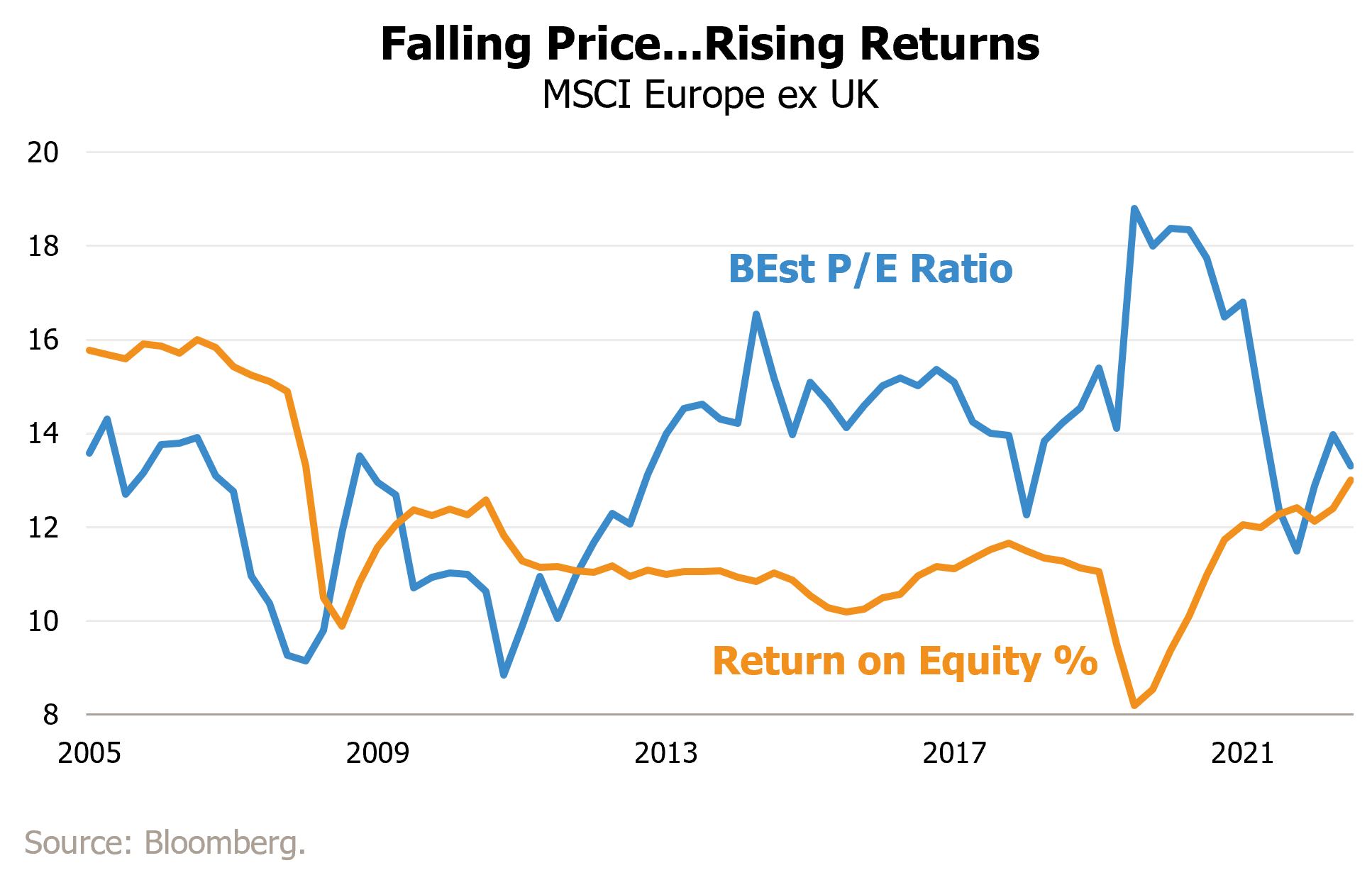

But while the transformation of the European economy Years of being passed over means the Europe ex UK index was in many ways left behind. The result is that, the average return on equity (RoE) for the index is being driven higher, particularly by the top 10 largest stocks which have an average weighted RoE of 40%. Meanwhile the index trades on only 13.3x price/earnings (PE), very close to its twenty year average, whilst as the chart shows the RoE across the whole index is currently at its highest point since 2008. We see a likely medium term valuation re-rating story for Continental Europe which is largely being ignored, driven by the likely continued improvement in Returns. Simply put, Europe is the home to an increasing number of great companies.

Well-positioned for change

We’ve continue to make plenty of changes to the JOHCM Continental European Strategy to make sure we’re well positioned for the upside, not least in embedding exposure to these key European themes in the heart of the portfolio.

We believe the regeneration of Europe is here to stay. Greater global exposure, decarbonisation and digitalisation are enduring themes, here for the next 10—20 years. Investing in the right way offers exposure to a once-in-a-generation transformation of the world’s largest economy.

Source for all data: JOHCM & Bloomberg (unless otherwise stated.)

Disclaimer

Professional investors only. This is a marketing communication. Please refer to the fund prospectus and to the KIID / KID before making any final investment decisions. The investment promoted concerns the acquisition of shares in a fund or the investment strategy and not the underlying assets. Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. The information contained herein including any expression of opinion is for information purposes only and is given on the understanding that it is not a recommendation. The information in this article does not constitute, or form part of, any offer to sell or issue, or any solicitation of an offer to purchase or subscribe for any funds or strategies described in this article; nor shall this article, or any part of it, or the fact of its distribution form the basis of, or be relied on, in connection with any contract.

With inflation continuing to soften, and growth returning, European valuations look still more attractive

Declining inflation and an improved outlook for interest rates are lifting European equities

Rates continue to rise even as Inflation continues to ease

Despite challenging macro conditions, earnings growth suggests a positive outlook for equities

A looming recession implies a bias toward defensives, but new infrastructure implies cyclicals - how has Paul Wild positioned the strategy?

For a better experience, we recommend viewing this website in landscape orientation.