See all results for ''

In late 2018, friends forced me to watch the movie ‘Crazy Rich Asians’. Not my genre of choice. Many friends and acquaintances who had never visited Singapore gushed about the pristine, manicured and glitzy playground for the ultra-wealthy. I tried to erase their misguided notions, citing anecdotes, quoting statistics and describing on-the-ground realities. I argued my case that movies are figments of someone’s imagination; they take liberties with the truth and create fantasies. Singapore may or may not be the ideal city-State to live in, but that movie did not represent reality. Today, I have revised some of my previously held beliefs.

I lived in Hong Kong between 1997 and 2007. Since moving to Singapore, I can attest to the animated debates with citizens and residents from each city on the merits or otherwise of both. During my Hong Kong days, that city was edgy, booming economically, outright entrepreneurial, a freer society in every respect. It possesses sublime hiking trails accessible 15 minutes from the heart of the city and enjoys a change of seasons to boot. Singapore’s reputation then was of a sterile ‘nanny’ State. A country with extremely competent elites who guided policy and sometimes bent economics to their will. After all, this island has no natural resources yet achieved such success as a society. Singapore was the underdog in a constant competition for talent and business.

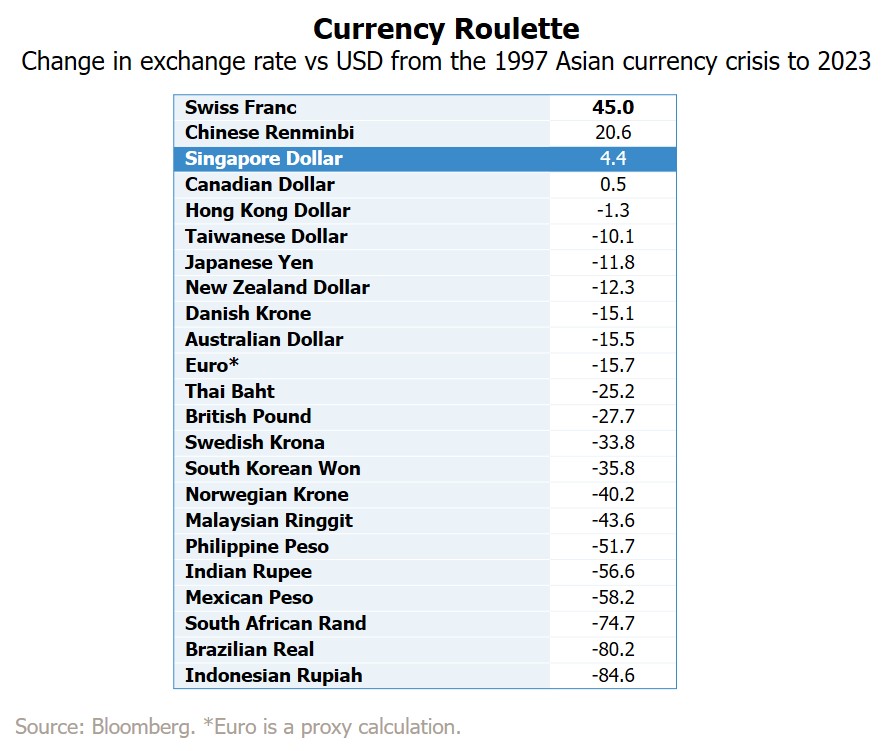

That reality was changing slowly but in my view it has morphed completely since 2019. The crackdown by mainland China on HK’s protesters clamouring for democratic institutions and a more open civic society was relentless and inhumane. China’s irrational zero-COVID shutdowns and harsh quarantine further damaged HK’s reputation as a business centre. Many HK residents moved to Singapore during 2021 and 2022. Some mainland Chinese (with means) frustrated and exhausted by China’s policies moved to Singapore too. Geopolitical tensions between the US and China on Taiwan, influenced several Taiwanese (and maybe some Chinese citizens) to reevaluate their own future or rearrange the domicile of their financial savings. Singapore’s robust institutions, especially the Monetary Authority of Singapore’s (MAS), and the rule of law (as opposed to rule by law in China) have fuelled a surge of immigration by the super wealthy to this island.

We are amidst cataclysmic changes in banking. The demise of Credit Suisse and Silicon Valley Bank has refocused our minds on regulations, capital adequacy and most importantly risk management. The risk of contagion and bank runs is high. When public confidence is fragile, technological advances allow funds to be withdrawn and moved in seconds, the role of prudence amongst regulators is paramount. We cannot claim that Singapore is immune – after all the reputation of the Swiss for banking was pristine till March 2023. We need to remain guarded at every stage, yet following the Asian financial crisis in 1997/98, banking regulations in Asia were strengthened. In Singapore, the MAS has emphasised risk management and demanded much higher capital ratios than those required by accepted global standards. This emphasis on fortress balance sheet and prudence in risk management has served the city state well through several financial crises.

The MAS still allows experimentation in new industries, knowing full-well the risk of failure. A ‘sand-boxing’ regulatory environment allows financial technology (fintech) companies to test new products or services in a controlled environment without having to comply with all regulatory requirements upfront. This allows them to innovate and develop new products and services, while MAS oversees the process to protect consumers and maintain the stability of the financial system. If successful, the fintech companies may be granted full licences. There have been blow-ups - Three Arrows (the crypto hedge fund) and Terra Luna (the stable coin) were both founded and based in Singapore. Yet the affect on the mainstream financial system was negligible.

Besides, Singapore in my view is a major beneficiary of the China + 1 trend in rebalancing global supply chains. The US-China trade war and COVID-era supply chain disruptions forced companies to rethink China’s role as a manufacturer of goods. Yet we overlook financial services - an equally important adjunct in a globalised world. As a business we need safe and efficient banking systems, well-capitalised insurance firms and robust legal infrastructure. For family offices, high net worth individuals and retail participants, we look for stability of currency, rule of law, a transparent jurisdiction for arbitration and, increasingly, personal security. On all these counts, Singapore is one of the best in the world and a hub for global wealth management.

Companies like DBS Bank are witnessing significantly better opportunities for growth, helped by Singapore’s reputation as a financial center. Founded as a state-owned bank, they had a dour reputation for decades. Under their current CEO, Piyush Gupta, and his team, DBS has undergone a digital transformation over the past few years. Already the dominant bank in Singapore and to some extent around the region, their competitive advantage lies in relatively stable deposits, ample liquidity and prudent provisioning norms.

It's not all smooth sailing for DBS – recently they had a second outage of their online service access. While disappointing, what is instructive is to observe MAS’s response to DBS’s first disruption in November2021. They forced DBS to hold US$625m of additional capital. As a shareholder that certainly hurts – more capital equals less leverage and probably lower earnings. Yet from a systemic perspective it is a signal that the MAS sends – if you are lacking in risk management, we will impose capital costs which affects shareholders but bolsters the system.

A multitude of family offices and HNI’s relocating to Singapore combined with the travails at competitors such as the Credit Suisse private bank are only aiding them further. Here too there are downsides – cost of living in Singapore has risen sharply. Rental costs are up on average by 40% in the last year, reflecting increased demand but also lingering delays from Covid-affected supply constraints. In my view, this is a process of adjustment as the economy adapts to changing drivers of growth. Even here, a parallel to Switzerland can’t be missed – for decades, that country remained one of the most expensive places in Europe. If history is a guide, this shock to the Swiss banking system will only reinforce this trend to the benefit of Singapore.

Disclaimer

For professional investors only. This is a marketing communication. Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. The information contained herein including any expression of opinion is for information purposes only and is given on the understanding that it is not a recommendation. Portfolio holdings are subject to change at any time and are not recommendations to buy or sell any security

Following the collapse of SVB and the risk of a banking crisis, the Fed may need to choose between price stability and financial stability

Sub-24 hour S&P 500 options are a sign of the equity market’s constant drive to short-termism. Is patient, long-term investment still justified?

When Adani came into the India index, passive funds had to buy the stock, driving up the price. As the price has fallen, reducing the weighting in the index, they have had to sell.

For a better experience, we recommend viewing this website in landscape orientation.