See all results for ''

One adage holds true across market cycles. The leading theme, sector or country that defined a bull market rarely leads the next bull market. The 1990s technology bubble gave way to commodities, housing and emerging markets in early 2000s. In 2008/9 the baton passed to disruptive (in many cases loss-making) technology, ESG and alternative energy themes, mostly concentrated in the US.

Globally, ‘inflation higher for longer’ implies lower stock prices ahead due to higher rates, challenged earnings growth and lower valuation multiples. Conversely, for the camp that believes the peak in inflation is behind us, there might be a respite from interest rates, but a looming recession could lead to lower earnings.

In Asia, we are clearly in a bear market. A strong US dollar, higher energy costs, rising rates, slowing growth and geopolitics have all played a part. With a myriad of macroeconomic cross currents, it would be arrogant on my part to opine with any confidence that this bear market is over. However, sentiment towards Asia is deeply pessimistic, accompanied by a pall of risk aversion. Yet I find several opportunities to invest in. I do think the time to invest in Asia is close. It’s difficult to call the exact low but adding to your allocations over time is the ideal way of minimising sharp drawdowns.

In my view there are three reasons to invest in a stock. First and foremost, valuations – stocks must be cheap, preferably on an absolute basis. After a decade of extended valuations, relative valuations are tainted by the era of free money. Yet cheapness by itself hardly qualifies for buying a stock. They could turn out to be either ‘value traps’ or stay cheap for a long time.

The second precondition is a demonstrated improvement in the trajectory of cashflows likely to lead to a stronger balance sheet. It demonstrates hard decisions made by management to either improve or right-size the business. Better working capital management, expense control, cuts in non-critical capital expenditures and deferment of expansions are excellent barometers of positive cashflows.

If you find a combination of these two conditions, the chances of losing too much money are low. The third element is market liquidity. Something must trigger investors en mass to buy that stock. Those triggers vary, but underlying a trigger is a rush of liquidity. In a benign liquidity environment, valuation multiples expand. When liquidity is ample and sustained, we have a bull market and sometimes a bubble.

Humans, by nature, test their endurance of mental, emotional, and physical limits. Little did I anticipate that China’s zero-COVID policies would turn into just such a test. Since March 2022, I have added to our China holdings while opining that India was just too expensive for comfort. So far, I have been wrong. Yet when you peel the onion, stocks in China already meet two of the three conditions I mentioned above.

Take Budweiser APAC (Bud), which is one of our top 10 holdings. The parent, a multinational, has decades of operating experience across countries through inflation, deflation, booms and busts. That management expertise is essential in Asia to deal with challenging conditions. Bud operates predominantly in China (largest part), South Korea and India. Bud has focused on expanding its footprint in China to more cities, driving premiumisation and managing costs. Their cashflows are stellar.

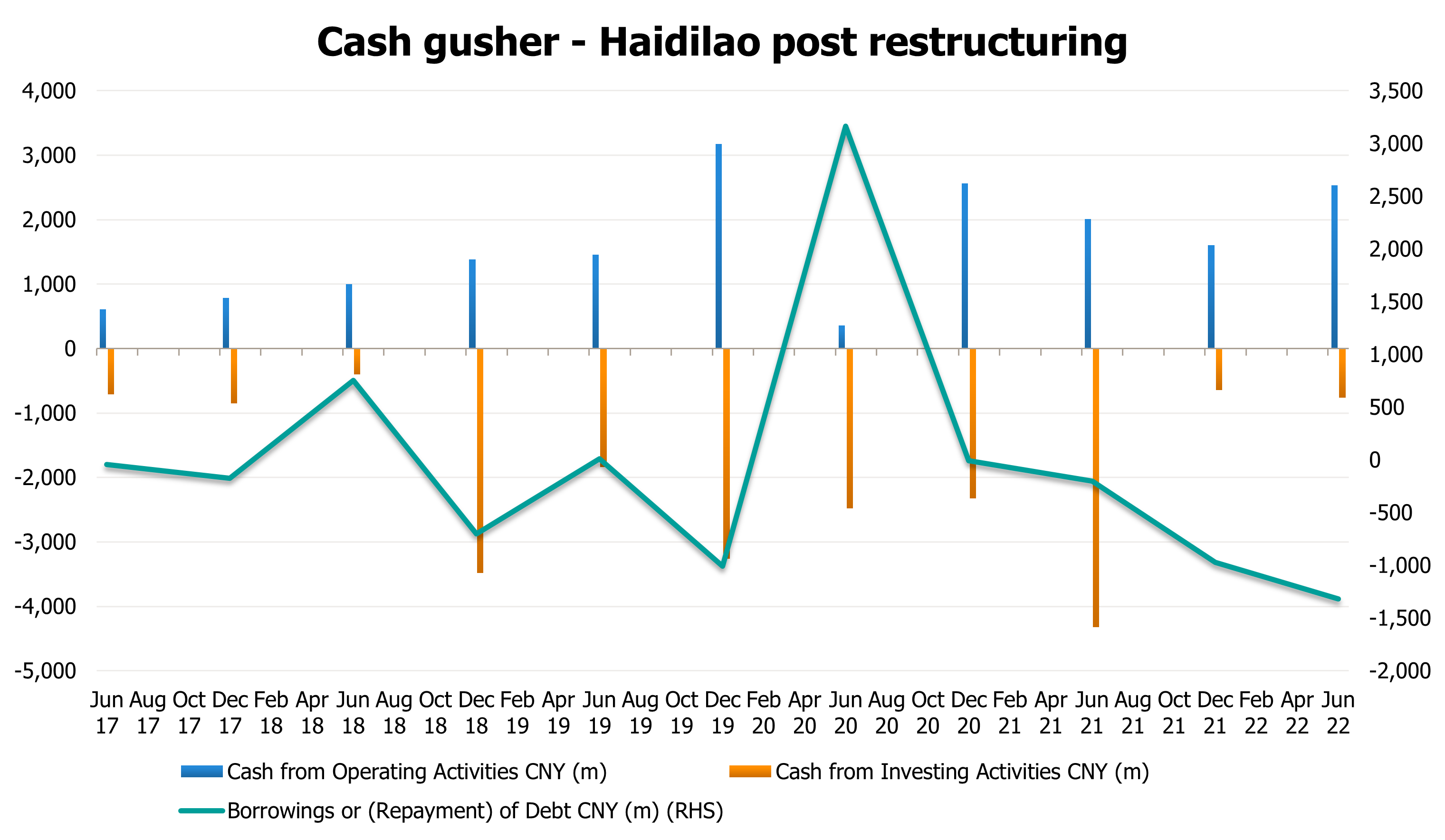

Haidilao, a hotpot restaurant chain, has reorganised its business. It has reduced headcount and store count by approximately 20%, curtailed expansion, relocated stores and decided to spin off its international operations as a separately listed business to shareholders. By right-sizing its business and generating cashflows in tough times, it bought back 20% of its outstanding US dollar bonds. In my opinion, Haidilao is primed for substantial operating leverage whenever ‘dynamic COVID’ becomes undynamic.

Source: Bloomberg

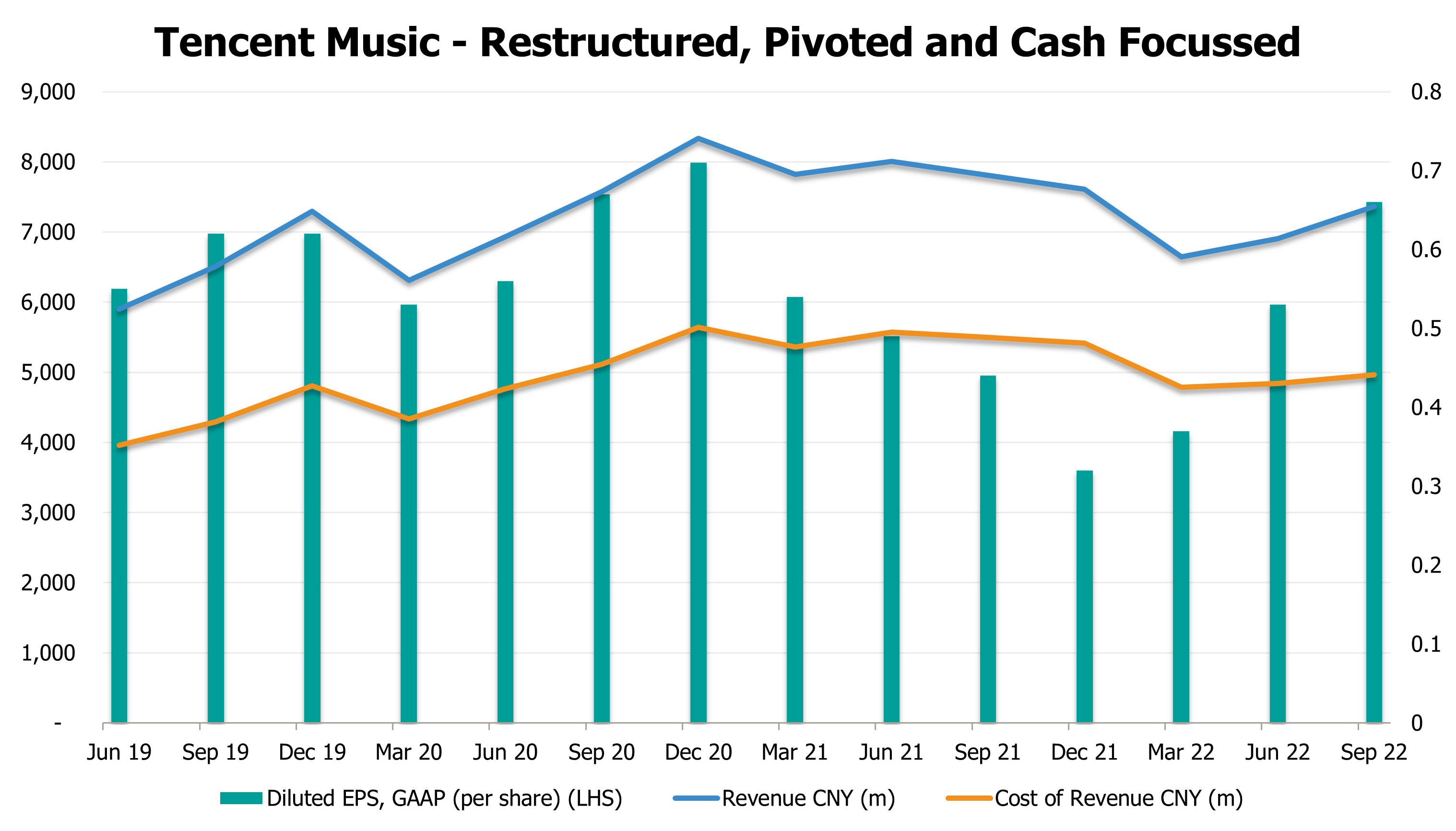

Tencent Music (owned by Tencent) is the ‘Spotify of China’. Regulatory clampdowns badly affected the social entertainment music arm of its business. In the past 18 months, its core subscription business has cut user acquisition, sales and marketing expenses by well over 40%. The number of paying customers rose from 51.7m in Q3 2020 to 85.3m in Q3 2022, while average revenue per unit is growing at over 7%. The company recently announced a US$1 billion buyback.

Source: Bloomberg

I could cite more examples, but hopefully, the message is clear. During tough times, some businesses in China have done the right things. Our screening process and analytical overlays are directed at finding those companies which have a potential for a rebound while doing what is critical for us – generating cashflows well above pre-COVID levels. These stocks are cheap and we need patience. China certainly was nowhere close to the leader board in the past bull run. What should also be obvious is that many of these companies are not the leaders of the past bull run and are not the heavy index constituents you might think of. With a rapid U-turn from an absurd policy, the next four to six months could see extensive waves of COVID infections and mortality. There will be very few positive headlines, and it will likely spur the authorities to counter by focusing on the economy. Could that be the trigger of liquidity needed to reset valuations?

Samir Mehta is senior fund manager on the JOHCM Asia ex-Japan Fund. For more information, please click here.

Disclaimer

For professional investors only. This is a marketing communication. Information on the rights of investors can be found here. The registrations of the funds described in this document may be terminated by JOHCM at its discretion from time to time. The investment promoted concerns the acquisition of shares in a fund and not the underlying assets. Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. Emerging Markets may have less stable legal and political systems, which could affect the safe-keeping or value of assets. Investments include shares in small-cap companies and these tend to be traded less frequently and in lower volumes than larger companies making them potentially less liquid and more volatile. Investments include shares in small-cap companies and these tend to be traded less frequently and in lower volumes than larger companies making them potentially less liquid and more volatile. The information contained herein including any expression of opinion is for information purposes only and is given on the understanding that it is not a recommendation.

Until recently, the consensus was that China would decouple economically from the developed world. Now we know the separation is not economic but ideological

Higher US interest rates could present significant upside for Asian equities

Conditions in Asia are considerably different to those in the US

For a better experience, we recommend viewing this website in landscape orientation.