See all results for ''

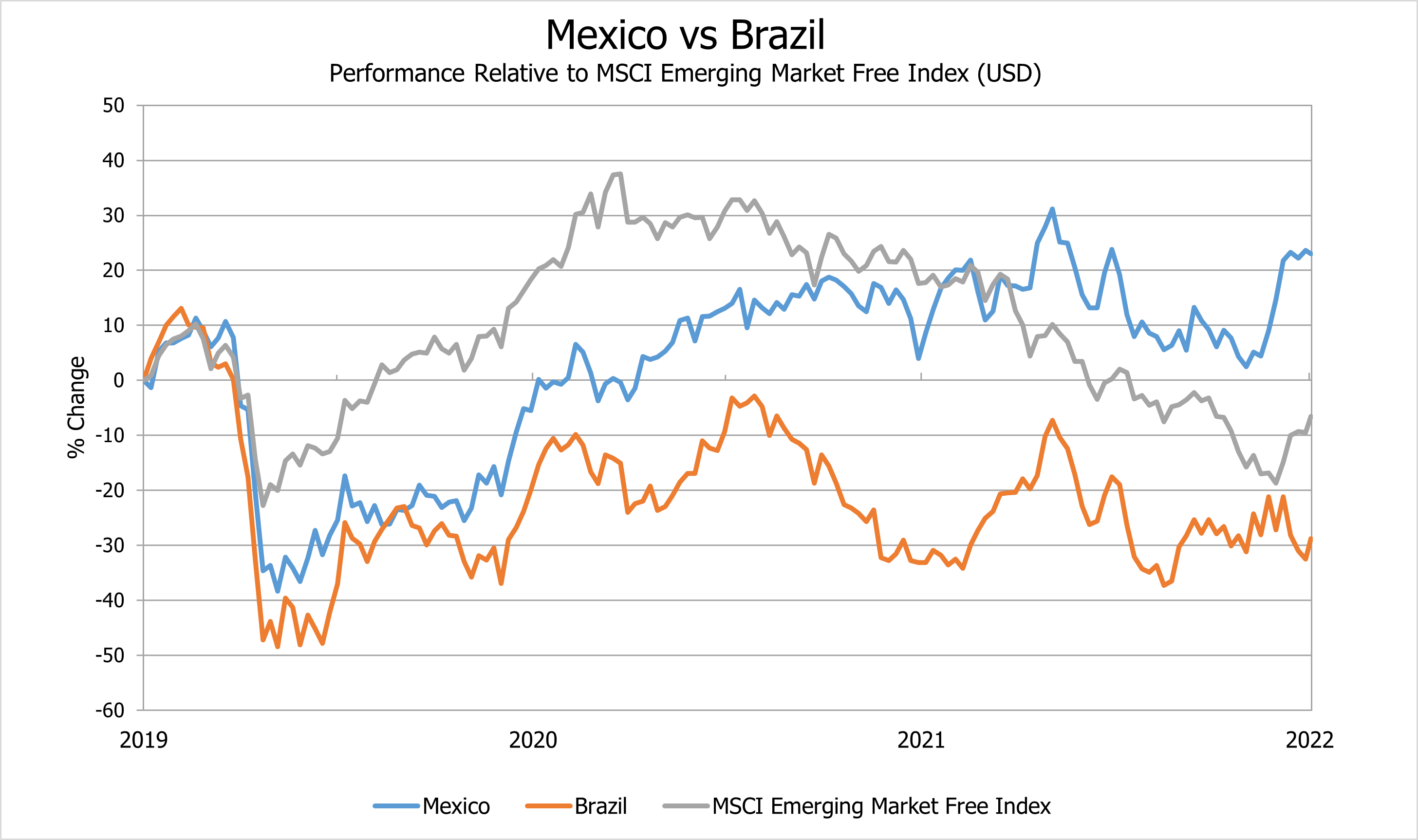

First, we must start with some numbers. One of the several paradoxes of the markets in the last couple of years is that, beneath the short-term volatility, we could sometimes find slightly more hidden, blurred, but more stable long-term trends. The performance of Brazil and Mexico have clearly demonstrated that they are on different paths to other markets. This is a common occurrence in emerging markets, as often some ‘pairs’ of countries are played against each other, India and China, for example.

Source:Bloomberg

If we look at Mexico, we see that the economy has grown considerably more than other markets, while equity valuations have improved relative company earnings. Notably, Brazil is still among the best performing markets in 2022, despite a significant fall triggered by Lula da Silva’s stunning re-election as president. More importantly Mexico has significantly outperformed on a three- and five-year basis and you may ask yourself, how come? There are several reasons, some related to Mexico and Brazil’s peculiarities and some to the broader market.

A significant and new phenomenon is beginning to appear, so-called ‘onshoring’ or ‘nearshoring’ or even ‘friendshoring’. It involves business operations transferring to a nearby country, or to a friendlier one, in preference to more distant or more hostile alternatives. Mexico seems to be among the largest beneficiaries, followed by markets in Eastern Europe.

But again, this is not a new concept. In the 1990s, the North American Free Trade Agreement (NAFTA) encouraged free trade and led to a significant bilateral commercial relationship between the US and Mexico. As globalisation continued to flourish, Western nations took full advantage of China’s low-cost manufacturing base. This lasted until the late 2010s, when President Donald Trump came with the first formal pushback to the globalisation trend. This position has continued into Biden’s administration, with more barriers on China, including import bans of certain materials and prohibiting US citizens from working in Chinese firms.

For many years the world enjoyed Russia supplying discounted commodities, Germany providing reliable machinery and China manufacturing cheap goods. As a result, western consumers enjoyed cheaper finished goods. Supply-side shocks have broken the chain, accelerated first in the pandemic and then due to the war in Ukraine.

Of course, Saudi Arabia and other oil-rich states will always supply the world with more oil, Brazil will benefit from higher exports of food and metals, Japan will compete with Germany to provide more machinery - the list goes on. But Mexico enjoys the great opportunity of offering both a near and a friendly shore for businesses wishing to relocate supply chains from Asia, in particular from China. Researchers estimate that the opportunity could contribute an additional 9% to Mexican GDP, with a 30% increase in exports. I recently attended a Latin American conference, and the attendees were very excited, showing maps, investments in motion, and infrastructure projects directed towards warehouses and roads. A new and exciting twist to this emerging trend is Chinese and other Asian companies joining the migration and adding their own direct investment into Mexico. To paraphrase a well-known asset manager, this could be a small revenge for Mexico.

Let’s not forget Eastern Europe, a smaller manufacturing region working with the world’s second wealthiest player, Europe. It is an inevitable move. Importantly, more Eastern European countries have a second chance, particularly the Czech Republic and Hungary, as the premium in production and labour cost to China is still high. I often meet Chinese companies exporting to Europe, and I’m stunned when I hear how low their costs are compared to Eastern Europe. While Mexico may accrue most of the benefits of serving the United States, in Eastern Europe it will be more structured and spread out among a number of countries, not least as the Czech Republic can hardly compete on labour costs anymore. Bulgaria, Romania, Eastern Poland and, once peace is restored, parts of Ukraine will enjoy substantial manufacturing inflows as more countries diversify their supply chains. Additionally, several initiatives are already working, such as the ‘3Seas’, and several Ukrainian funds are being gathered to help finance the country’s reconstruction. Curiously enough, such moves could also help with better company-level ESG scores.

Even if the war in Ukraine ends soon, a return to the old patterns is unlikely, certainly not to the same degree. Whether you call it national security or political and economic diversification, some redundancy is already being built into the system, and, unfortunately, that has a terrible impact on costs and inflation. But that is how economies build reliability, too. And that is how you build new regional chains, and that newly built capacity and redundancy increases the whole pot. There is no doubt that Brazil will benefit from Mexico’s nearshoring and that other Asian countries will be included in the newly formed regional chains moving out of China.

Hence, to finish with a view of our latest portfolio changes, we are fully employing our famous and robust dual philosophy, adding more to Mexico, while taking some profit in Brazil. We have also built a position in Indonesia and now look to reopen plays in Thailand and Malaysia. But of course, we are rotating into China, getting a bit more aggressive with the portfolio’s recovery stock exposure.

Disclaimer

For professional investors only. This is a marketing communication. Information on the rights of investors can be found here. The registrations of the funds described in this document may be terminated by JOHCM at its discretion from time to time. The investment promoted concerns the acquisition of shares in a fund and not the underlying assets. Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. Emerging Markets may have less stable legal and political systems, which could affect the safe-keeping or value of assets. Investments include shares in small-cap companies and these tend to be traded less frequently and in lower volumes than larger companies making them potentially less liquid and more volatile. Investments include shares in small-cap companies and these tend to be traded less frequently and in lower volumes than larger companies making them potentially less liquid and more volatile. The information contained herein including any expression of opinion is for information purposes only and is given on the understanding that it is not a recommendation.

The strength of the US dollar has impacted emerging market currencies, delayed expected interest rate cuts and reduced returns to international investors

Remittances have been the largest source of external finance flows to developing countries ex-China

The dollar is stronger than it’s been in 20 years. What’s the impact on emerging markets?

Rates in Mexico and Brazil are coming down. Despite cautious guidance, we believe further cuts will be ahead of consensus

As investors move away from China, we look at some interesting alternatives

For a better experience, we recommend viewing this website in landscape orientation.