See all results for ''

2023 was dominated by the extraordinary performance of a handful of US mega-caps. We expect 2024 to be a year of ‘vice versa markets’, when the stellar performers of last year are likely to fall back, while prospects look considerably better for some of the year’s underperformers.

Forecasts are better for emerging markets as North America’s relative fortunes decline. We expect the Bank of Japan (BoJ) to change its interest rate policy which should see the value of its languishing currency rise. And the tide could be set to turn for small and mid-caps, as they trade places with large caps.

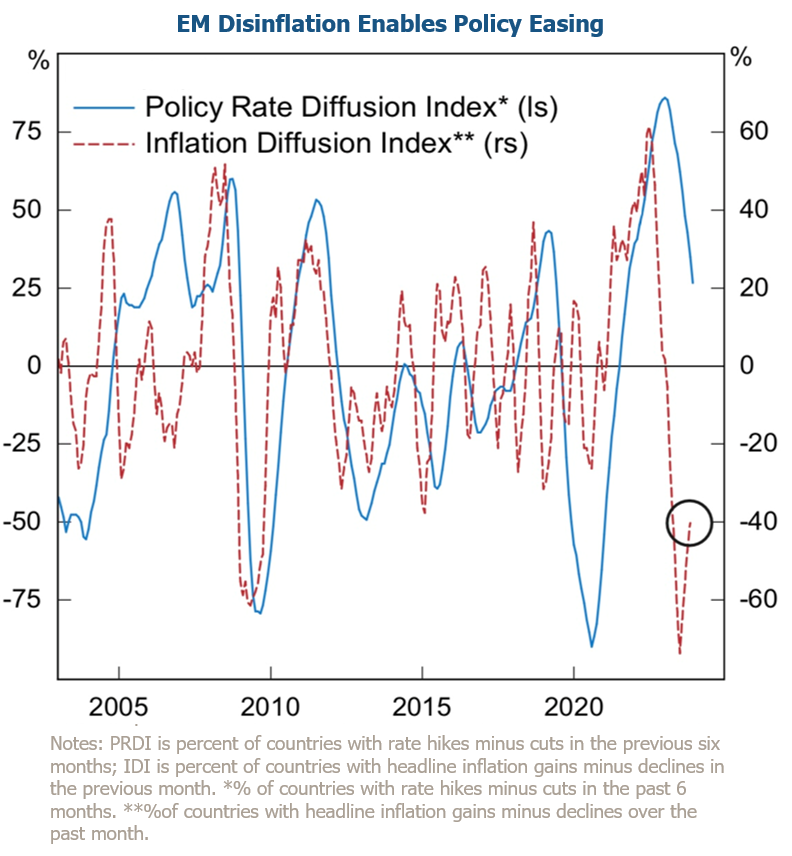

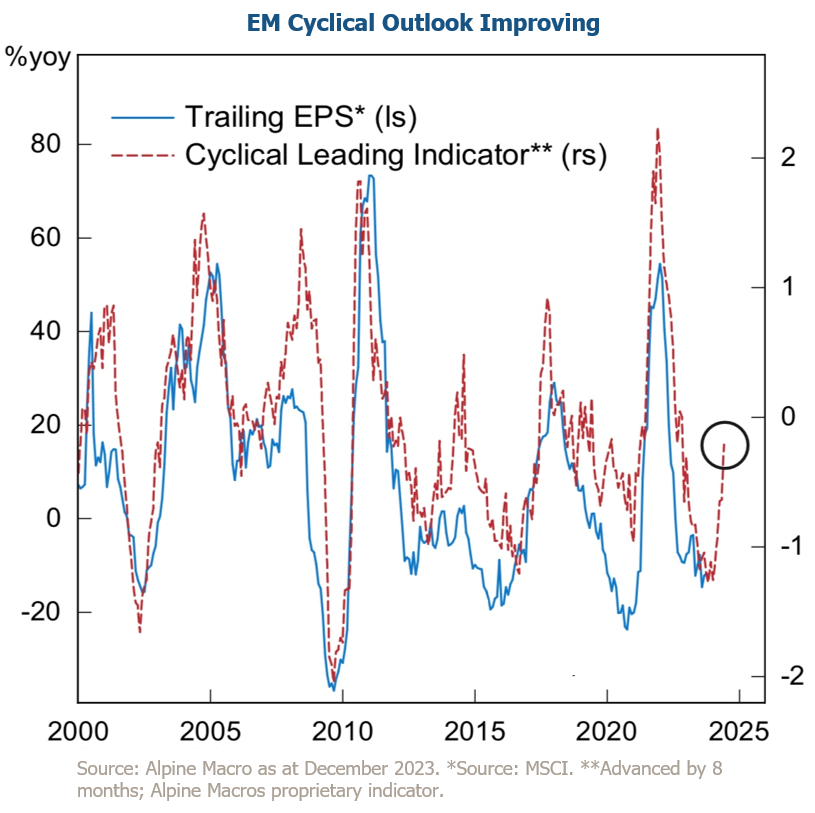

The recovery of emerging markets

2023 saw better than expected economic improvement in the US and deterioration in emerging markets. North America’s ‘Magnificent Seven’ outperformed the MSCI All Countries World Index by an astonishing 73%. Emerging markets languished down at the other end of the performance charts, trailing global indices, with China underperforming the MSCI All Countries World Index by 28%.

We expect this theme to reverse in 2024. The US is showing early signs of peaking, the Magnificent Seven are starting to look expensive, and we give them a 10% probability of repeating their 2023 outperformance. Emerging markets tend to perform better as interest rates fall and we’re already seeing strong recovery in emerging market cyclical lead indicators. We expect emerging market earnings to recover strongly too. Falling interest rates plus re-accelerating earnings growth sets emerging markets up for a better 2024.

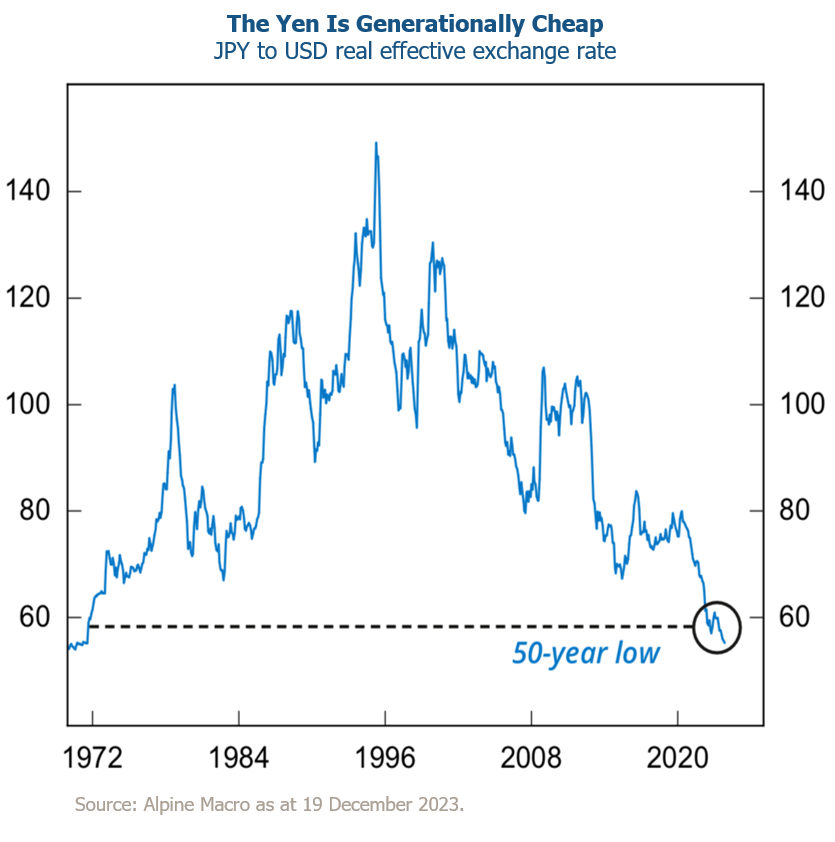

A resurgence of the Japanese yen

The Japanese yen is very cheap and we’re expecting it to rally this year. The value of the currency peaked in the nineties, but Japan’s negative interest rates took the yen to 50-year lows in 2023 (on a real effective exchange rate).

A change in policy should reverse the currency’s fortunes. The BoJ is the last central bank with negative interest rates and forecasters expect that to change in 2024, with profound implications for global fixed income, equities and currencies, including the yen.

Even if the BoJ doesn’t end negative interest rates, the Fed’s recent dovish pivot on rates and the BoJ’s loosening of yield curve control are both bullish signs for the yen over the year ahead. We believe that the worst of the currency’s weakness is over.

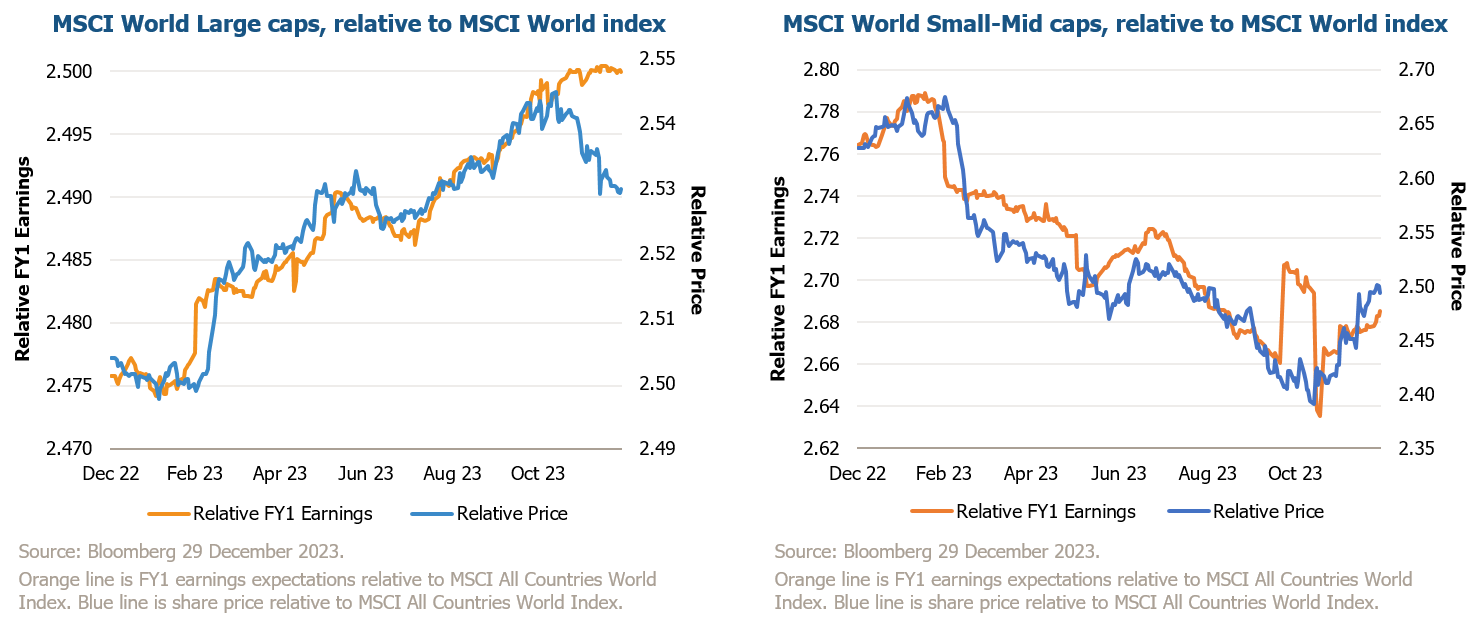

Large and small caps trade places

Large caps (above $50bn) had a strong year in 2023, with notable outperformance relative to the MSCI World index. The opposite was true for small caps, as they trailed the same index. But in 2024, that tide is set to turn. The 2023 Q4 peak for small-mid caps was driven by relative earnings and we think that’s the start of a new trend of superior relative earnings and price. Earnings and price performance is peaking for large caps and recovering for small and mid-caps.

The most likely scenario

Looking at the year ahead, we’re expecting a broadening bull market, with much better performance from emerging markets, the Japanese yen and small-mid caps. A bear market is not impossible, but for that to happen, we would have to see resurgent inflation and interest rates, or geopolitical escalation in the Middle East.

Disclaimer

Issued and approved in the UK by J O Hambro Capital Management Limited (“JOHCML”) which is authorised and regulated by the Financial Conduct Authority. Registered office: Level 3, 1 St James’s Market, London SW1Y 4AH. Issued in the European Union by Perpetual Investment Services Europe Limited (“PISEL”) which is authorised by the Central Bank of Ireland. Registered office: 24 Fitzwilliam Place, Dublin 2, Ireland D02 T296. References to “JOHCM” below are to either JOHCML or PISEL as the context requires. Perpetual Group is a trading name of JOHCML and PISEL.

This is a marketing communication.

The distribution of this document in jurisdictions other than those referred to above may be restricted by law (“Restricted Jurisdictions”). Therefore, this document is not intended for distribution in any Restricted Jurisdiction and should not be passed on or copied to any person in such a jurisdiction.

The investment promoted concerns the investment strategy and not the underlying assets.

Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested.

Investing in companies in emerging markets involves higher risk than investing in established economies or securities markets. Emerging Markets may have less stable legal and political systems, which could affect the safe-keeping or value of assets.

Investments may include shares in small-cap companies and these tend to be traded less frequently and in lower volumes than larger companies making them potentially less liquid and more volatile.

The information contained herein including any expression of opinion is for information purposes only and is given on the understanding that it is not a recommendation.

The information in this document does not constitute, or form part of, any offer to sell or issue, or any solicitation of an offer to purchase or subscribe for any funds or strategies described in this document; nor shall this document, or any part of it, or the fact of its distribution form the basis of, or be relied on, in connection with any contract.

Telephone calls to and from JOHCML and PISEL may be recorded. Information on how personal data is handled can be found in the JOHCM Privacy Statement on its website: www.johcm.com

J O Hambro® and JOHCM® are registered trademarks of JOHCML.

Sources: JOHCM/MSCI(unless otherwise stated).

Certain information contained herein (the “Information”) is sourced from/copyright of MSCI Inc., MSCI ESG Research LLC, or their affiliates (“MSCI”), or information providers (together the “MSCI Parties”) and may have been used to calculate scores, signals, or other indicators. The Information is for internal use only and may not be reproduced or disseminated in whole or part without prior written permission. The Information may not be used for, nor does it constitute, an offer to buy or sell, or a promotion or recommendation of, any security, financial instrument or product, trading strategy, or index, nor should it be taken as an indication or guarantee of any future performance. Some funds may be based on or linked to MSCI indexes, and MSCI may be compensated based on the fund’s assets under management or other measures. MSCI has established an information barrier between index research and certain Information. None of the Information in and of itself can be used to determine which securities to buy or sell or when to buy or sell them. The Information is provided “as is” and the user assumes the entire risk of any use it may make or permit to be made of the Information. No MSCI Party warrants or guarantees the originality, accuracy and/or completeness of the Information and each expressly disclaims all express or implied warranties. No MSCI Party shall have any liability for any errors or omissions in connection with any Information herein, or any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

Japan's Surging Appeal as Investors Look for Diversification amid China's Economic Troubles

For a better experience, we recommend viewing this website in landscape orientation.