See all results for ''

Ouroboros – an emblematic serpent of ancient Egypt and Greece, represented with its tail in its mouth, continually devouring itself and being reborn from itself.

For all the market’s obsession on macro-economics, we often forget that one of the key determinants of a company’s success is its management team.

As active managers, we invest a reasonable amount of time trying to divine a company’s leadership, their strategy, industry dynamics and execution capabilities. That is easier said than done, yet I’ve learnt from experience that this aspect is critical to successful long-term investing. Understanding the management’s mindset towards capital allocation, revisiting their past decisions during tough economic conditions, juxtaposing those decisions with competitors’ responses and prevailing industry dynamics, can all suggest why there could be substantial divergences in business outcomes.

During the past three years, through and post-COVID, all of us grappled with some broad dynamics:

- Supply chain disruption and fiscal stimulation leading first to a demand revival and subsequently a slowdown in growth across most of Asia

- Cost and availability of capital, regulations, rationality of competitors; and management’s response to these challenges

There were lessons for all of us on how managements react across different industries and different countries, facing somewhat similar challenges. In that vein, I thought of presenting four companies in different industries, two of which we own in our fund, the other two I have never bought.

How do you manage when you’ve never really seen a slowdown?

The Chinese economy faces multidimensional challenges. Authorities have so far deployed neither monetary nor fiscal policies to turbocharge growth. Entrepreneurs in China, possibly for the first time in decades, face a sustained economic slowdown. As a management, your destiny is almost completely in the decisions you take.

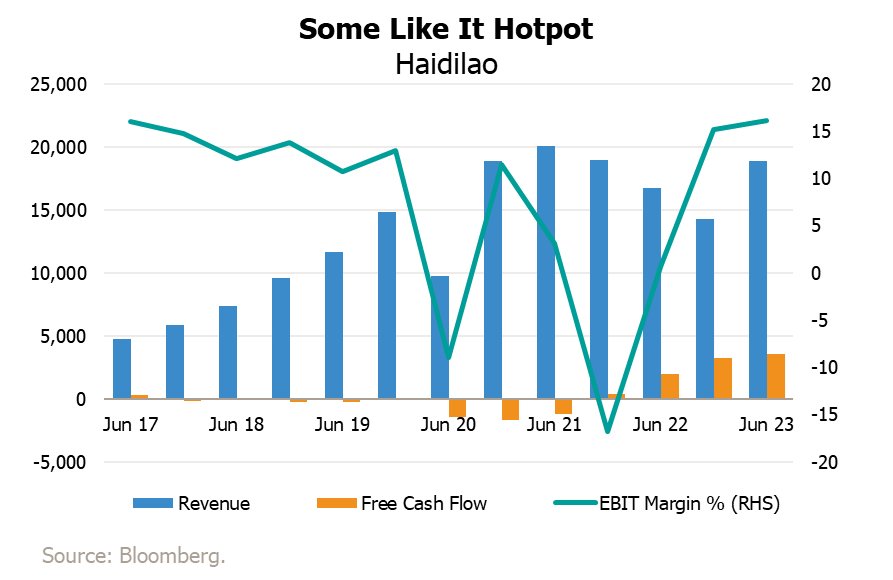

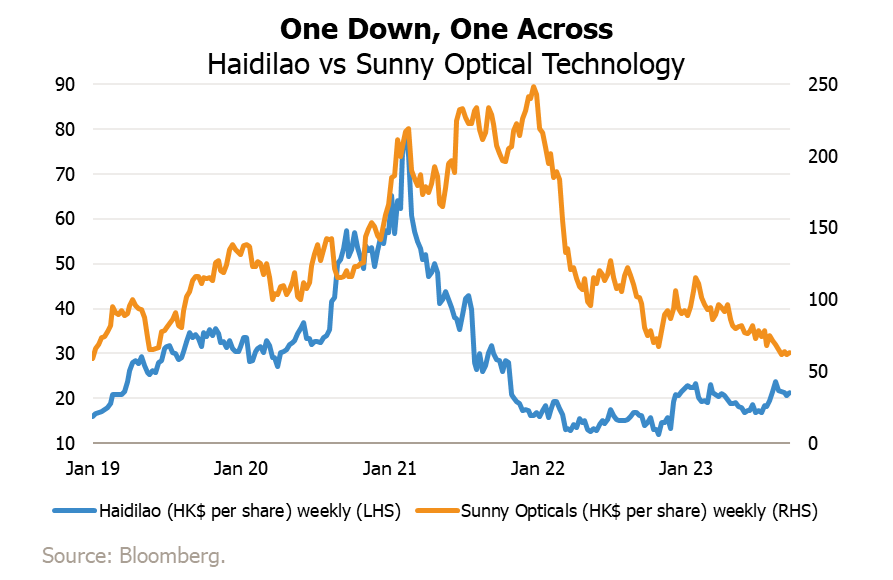

Haidilao, a popular restaurant chain in China specialises in hotpot (a communal meal where diners cook ingredients in a shared pot of simmering broth) faced a reckoning during the pandemic lockdowns. After nearly two decades of strong growth, business came to a near standstill. Haidilao management responded by shuttering nearly a fifth of their restaurants and let go more than a fifth of staff, something rare in China. Staff compensation structures were modified from fixed to mostly variable; they spun off their fast-growing but cash guzzling international business as a separate company and distributed the shares to existing shareholders. Their single-minded focus was on generating cash flows by right-sizing costs and bunkering down. With the cash on hand, they bought back a part of their outstanding US$ bonds to de-leverage their balance sheet. Through 2022, they drove efficiencies such that, when demand did return, there could be an explosion in profits.

That is exactly what happened in 1H2023. Haidilao posted a 12% lift in revenue compared to 1H22, and profits of CNY2.26bn (30% higher than the market’s expectations) compared to a loss in 1H22.

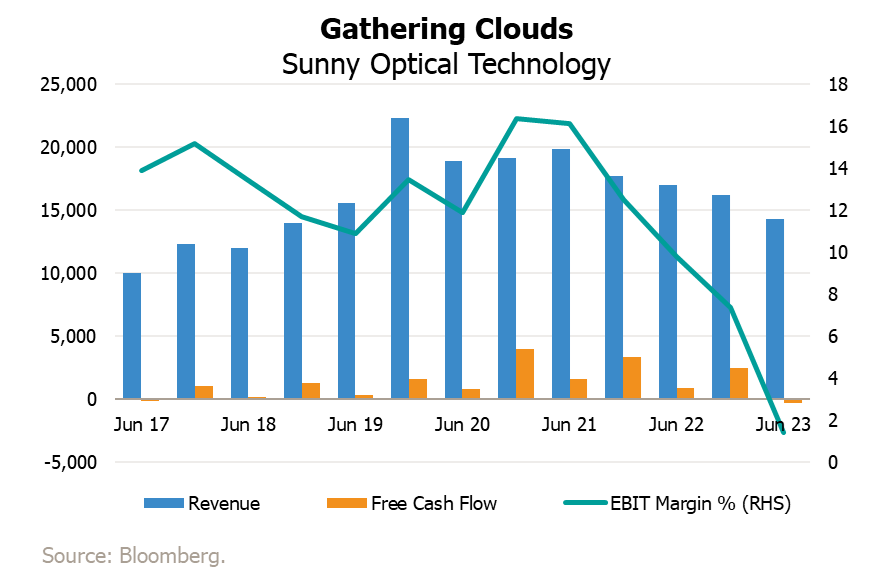

Contrast that to Sunny Opticals which makes optical components used in mobile phone cameras and vehicle lens sets. They are one of the largest suppliers to the global mobile phone industry. The last decade was an era defined by mobile phones and Sunny was one of the poster boys of that trend. However, growth rates in mobile phone handset sales have now plateaued as penetration levels across the world have risen sharply. One of their largest customers, Huawei, was caught up in geopolitics as the West backlisted and banned the use of Huawei equipment and devices. Sunny faces a more downbeat, and in my opinion, a more uncertain future. Yet management’s opinion is quite different. They are investing heavily in R&D and new capabilities to find new avenues of growth.

One area of focus is self-driving vehicles, which need lenses for the LIDAR components that help the vehicle understand its surroundings. Another is virtual reality headsets. Investing in R&D during a slowdown could be a good thing yet, in my opinion, they are driven by an inherent desire to grow at all costs. They do not want to reduce staff strength despite challenges, preferring to reassign them to different divisions. As a result, even as sales growth has fallen, their costs and investments have continued to rise to the detriment of margins and cash generation.

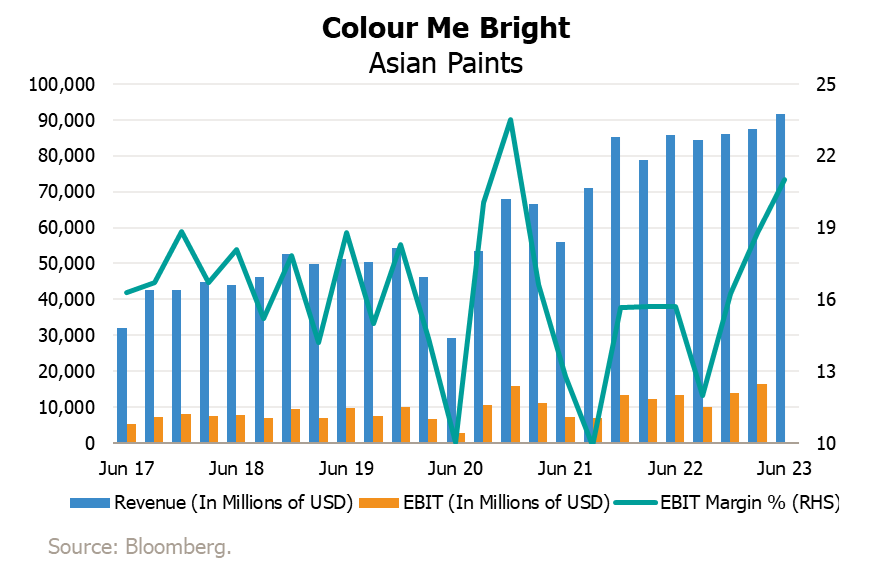

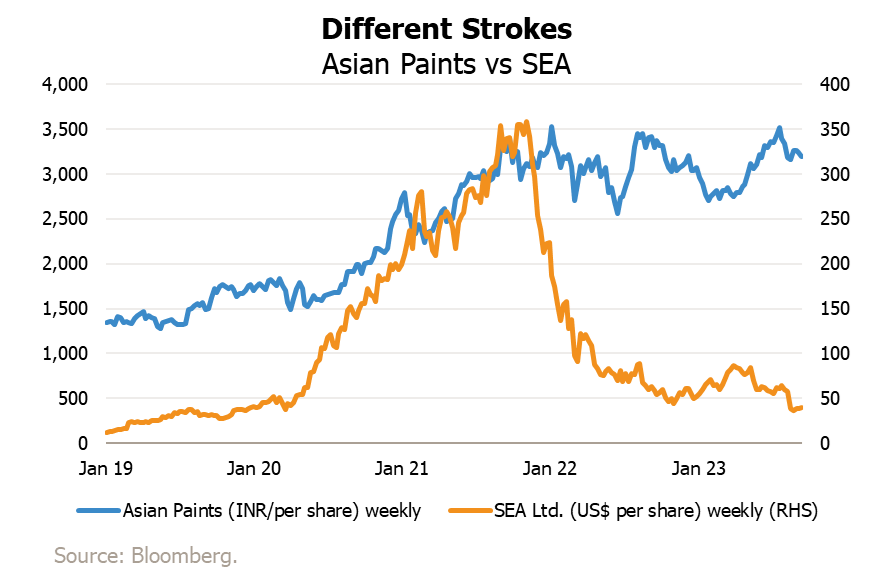

India, in contrast to China, is enjoying its moment in the sun as a confluence of events has sustained a better economic outcome compared to other Asian countries. Asian Paints is India’s largest paint company. Paint is unique worldwide among consumer goods; it has largely resisted digital disruption. Most consumer goods businesses have been disrupted by ecommerce, but paints as a category are still primarily bought by going to the store.

Asian Paints currently faces a different challenge. The company is one of a benign, highly profitable oligopoly. Attracted by this dynamic, one of India’s largest commodity-based manufacturing companies, Grasim Industries, is venturing into the decorative paints market. Grasim is at heart a commodity producer. For them capital expenditure is the solution to all problems. They have invested millions of dollars in the past three years to set up manufacturing plants to get a foothold in the industry. Asian Paints, recognising the nature of this competition, was well ahead of the curve. Going against the grain, they too have invested aggressively, building new capacity and investing in their brands.

Since their existing business is highly profitable, they have generated solid cash flows and built up a fortress balance sheet which will allow them to survive years of intense and in my view potentially irrational competition. The impact of this competition will most likely fall on the smaller competitors in the industry. The impact on Asian Paints, in my opinion, will be lesser than on competitors.

ASEAN (Association of South East Asian Nations) is a loose aggregation of disparate countries. It was founded in 1967 in an effort to prevent the spread of communism in the region. Then the scare was the USSR, today the scare is another communist nation, China. Over the years, the association has grown to include more countries which are increasingly clubbed together for investment purposes. I do not see any rationale for this, but several businesses do. Their logic is that this aggregation now has a population of over 600m and somewhat like the EU can be collectively a counterweight to China or India.

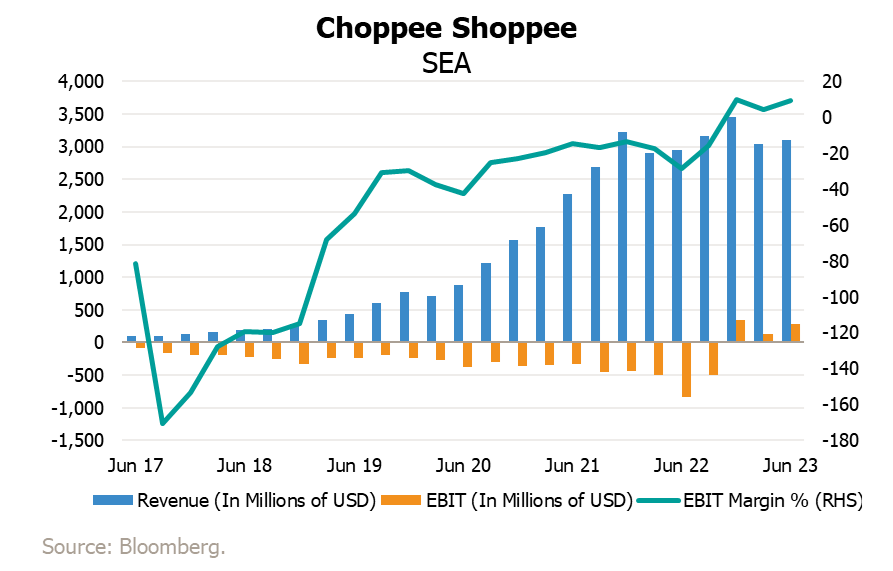

US-listed SEA is a market leader in e-commerce in Southeast Asia. It’s flagship app ‘Shoppee’ is probably the largest online shopping platform in the region. The stock skyrocketed during COVID, peaking above US$350, as consumers went online in droves. As was the wont of those times, SEA and its competitors subsidised customers, preferring to lose money on every trade in order to stimulate online shopping behaviour and cementing their brands. In 2022, as inflation roared back, stock markets wobbled and investors started focusing on profits rather than growth at any cost. SEA’s shares fell to around US$30.

Management’s response was a classic textbook one - to dramatically change strategy and control costs. They mandated all travel only in economy class. They even reportedly went to single ply toilet paper in the bathrooms. And for a while, it worked. SEA shares doubled from their lows of $30 to almost $60 as management prioritised cash flows and profitability.

Despite best efforts, they achieved fleeting profitability for just couple of quarters. Their competitors did not follow suit and SEA management has now decided that they cannot afford to lose market share. They reversed strategy direction again last quarter. Even though they might have wanted to do the right thing for us as shareholders, their competitors have different plans. The stock is back around US$36.

Contrasting fortunes

Our approach to owning stocks is to focus on cash flows, profitability, and high returns on capital employed. These four companies faced similar kinds of challenges but took completely different approaches.

Asian Paints is a good quality business run by management who understand the long-term growth dynamics of the country and their industry. Considering competitive changes to the landscape, they have reacted well in my view. No doubt they will see reduced profitability as Grasim competes with an approach antithetical to a branded business. Though time will tell, I do believe they have taken the right approach which will benefit shareholders in the long run.

Contrast that with SEA which unfortunately faces an environment in Southeast Asia with lower growth and fickle consumers while the competitive intensity they face, accelerates.

Sunny Optical continues to invest despite a fall in growth, margins, and profits – it seems to be their DNA to grow at any cost.

Haidilao management recognised that times have changed. They resized their business, by cutting expenses and capital expenditure; focused on cash flow, bought back some of their debt, and prepared themselves to be in a situation where things might remain tough for a prolonged period.

Management mindset, industry dynamics, nature of customers amid macroeconomic externalities make a big difference to business outcomes. It’s not difficult to guess which two of the four names I own in our fund.

Source for all data: JOHCM & Bloomberg (unless otherwise stated.)

Disclaimer

Professional investors only. This is a marketing communication. Please refer to the fund prospectus and to the KIID / KID before making any final investment decisions. The investment promoted concerns the acquisition of shares in a fund or the investment strategy and not the underlying assets. Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. The information contained herein including any expression of opinion is for information purposes only and is given on the understanding that it is not a recommendation. The information in this article does not constitute, or form part of, any offer to sell or issue, or any solicitation of an offer to purchase or subscribe for any funds or strategies described in this article; nor shall this article, or any part of it, or the fact of its distribution form the basis of, or be relied on, in connection with any contract.

The future of AI will depend on a global ecosystem

The comparison between China's profit-driven pragmatism and OpenAI's pursuit of AI dominance

The ramifications of tighter credit conditions, and the critical role of near-term cash flow generation over future earnings projections.

Equity markets might be roiling on the surface but there are islands of calm, and opportunity, if you know where to look

China’s heavy-handed attitude to Hong Kong, to Covid, to trade relations, is playing to Singapore’s reputation for prudence and rule of law

For a better experience, we recommend viewing this website in landscape orientation.