See all results for ''

There are multiple risks and questions regarding the near-term economic outlook.

Among the most significant changes has been the return of consumer price inflation. This is due to a combination of a squeeze on energy prices and a breakdown in supply chains. At around 7—8%, present and prospective levels of inflation are a concern and will pressure living standards.

Higher rates in combination with slowing growth is being billed as ‘stagflation’, the phenomenon that characterised the 1970s. But the comparison is inexact. Then, inflation above 20% a year was wiping out savings, while large swathes of British industry were state-owned, uneconomic and in the process of shedding millions of workers.

That is not the current situation, where employment is firm, incomes are rising, savings are significant and far from facing a sweep of bankruptcies, UK companies are generally in good financial shape. There are also some mitigants to the cost-of-living pressures – over £200bn of excess savings, the rise in incomes (c. 5-6% this year in the UK) and likely further government action to assist households to offset the energy cost increase. The universal bearish commentary does not mention or discuss these mitigants.

The rise in bond yields linked to the rise in inflation has caused a material rotation in global stock markets – ‘long-duration’ growth stocks have collapsed with the Nasdaq down by 25% year to date. The fall in Amazon this year, which is in line with the fall in the Nasdaq, is itself equivalent to the FTSE 100 falling 14%. This observation highlighting the large market caps of these stocks, driven by high valuations, should raise alarm bells.

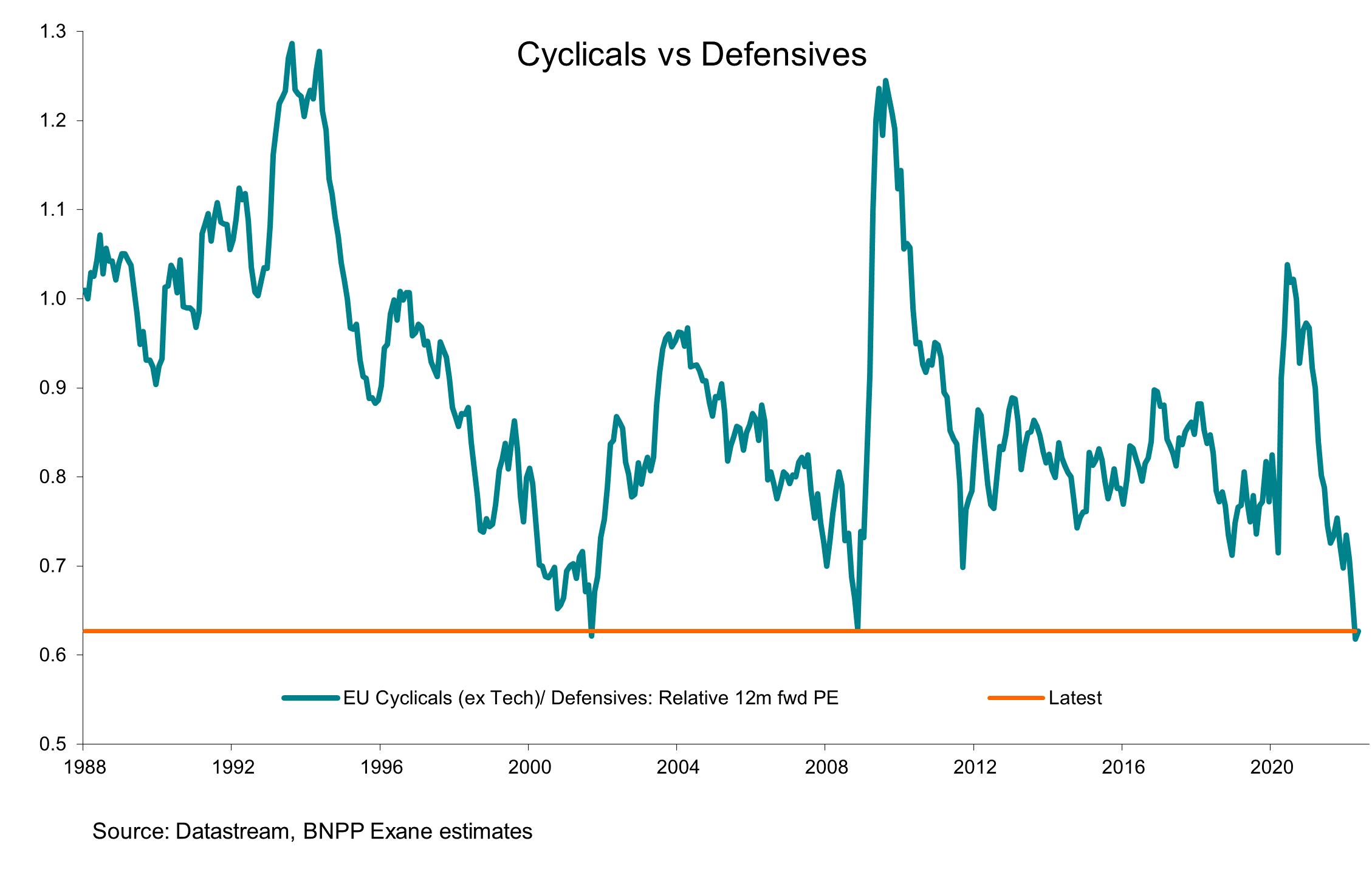

Abandoning growth, investors have rushed to commodities, for obvious reasons, and to defensives. This may be understandable as an immediate, knee-jerk response to the prevailing risks, but if we look at the chart below (showing defensives vs cyclicals) we can see the rotation within the market has reached extremes associated with previous risk-averse events (eg the Lehman collapse, 9/11 amongst others).

The largest seven defensive stocks – AstraZeneca, GlaxoSmithKline, Unilever, Diageo, Reckitt Benckiser, BAT and Imperial Tobacco now make up nearly a quarter of the UK market. AstraZeneca is also close to returning to a market capitalisation equal to the entire UK quoted banking sector. This cohort of stocks trade on c. 20-25x price earnings (PE) ratios. Unlike other long-duration stocks which have fallen materially year to date, as interest rates have risen, defensives in the UK market have remained robust.

At some point, just as in 2009 and following the successful roll-out of vaccines in 2020, there is likely to be a rotation back, given how distorted the market valuation structure is. No one knows what will cause that – which is the same in every market cycle, but possible drivers could be a peak in inflation, the end of the Ukraine conflict, a bid for a large cyclical UK company or just valuations for cyclicals becoming too low. This is the time to be selling defensives and buying high quality franchises in the rest of the market. The latter is where the Fund is positioned.

Below are some stock examples that bring this valuation gap into sharp focus. All are owned by the Fund.

Vistry (housebuilder & partnership homes) trades on a PE of 6x and has a yield of 8%+. Given its tangible book value, and with no debt, in our view it is likely to attract private equity interest. We would value the housebuilding side of the business at a price-to-book around 1, compared to a medium-term average for the sector nearer to 1.5 . The partnership business, equally, in our opinion, should be on a PE of around 15x. Taken together, this suggests a value of double the current share price.

Barclays, which in common with all banks, materially beat Q1 profit forecasts, with net interest income margins rising (as interest rates rise), costs under control and excess credit provisions / and capital trades on a PE of 6x and less than half its tangible book value. It yields 5-6%.

DFS which now has a market share of over 35% and is expanding as others leave the market. It is moving into tangential areas (eg beds) and has just paid a special dividend alongside a share buyback. It is trading on a PE of < 6x.

ITV, which following a record year ever for advertising in 2021, the company announced an investment to accelerate growth. The stock trades on a PE of c. 6x and yields more than 6%. If we value its studios (ie content business) at 10x EBITDA (lower than peers) the large broadcast business would be valued at less than zero.

The common theme in the above examples is a PE of 6x or less, a yield of 6% or more, safe balance sheets, managements that are executing and forecasts that are prudently set to reflect the wider risks. As we have recently discussed this in the new JOHCM Cool Britannia blog (see here) these valuations seem absurd. Contrast this to the valuation of the defensives that dominate the UK indices as noted above. The distorted valuation structure of the market is providing one of those (rare) moments – a major opportunity to buy UK value. This is also evident in the Fund dividend yield which is 5.5% for 2022 with close to half the holdings in the Fund currently buying back shares.

James Lowen and Clive Beagles manage the JOHCM UK Equity Income Fund. For more information click here.

Sources: All data JOHCM and/or Bloomberg unless otherwise stated; company data from company accounts

Disclaimer

For professional investors only. This is a marketing communication. Information on the rights of investors can be found here. The investment promoted concerns the acquisition of shares in a fund and not the underlying assets. Past performance is no guarantee of future performance. The value of an investment and the income from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested. Investing in companies in emerging markets involves higher risk than investing in established economies or securities markets. Emerging markets may have less stable legal and political systems, which could affect the safe-keeping or value of assets. Investments may include shares in small-cap companies and these tend to be traded less frequently and in lower volumes than larger companies making them potentially less liquid and more volatile. The information contained herein including any expression of opinion is for information purposes only and is given on the understanding that it is not a recommendation. The registrations of the funds described in this communication may be terminated by JOHCM at its discretion from time to time.

The rotation from financials and cyclicals to defensives has reached an extreme last seen following the collapse of Lehmans

Latest comments from our UK equity income fund managers

For a better experience, we recommend viewing this website in landscape orientation.